70% Tax Credits

Your guide to tax credits at Good Samaritan

Through the Neighborhood Assistance Program Tax Credit, you can enjoy a direct credit of 70% of your donation on your Missouri income taxes. These credits are available to corporations and individuals in the state of Missouri that have a business tax liability (Farmers, Landlords, Small-business owners, and more)

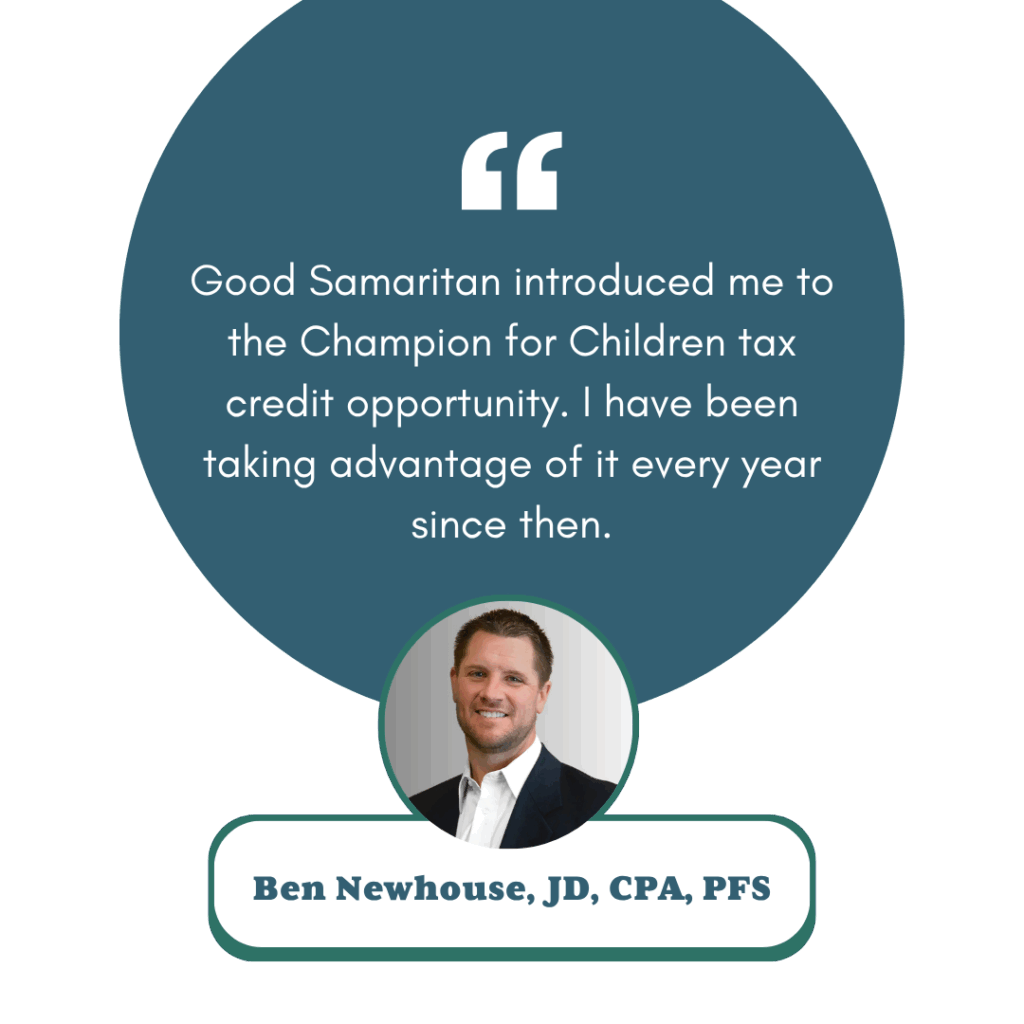

Your tax-deductible donation to Good Samaritan may be eligible for 70% tax credits through the Champion for Children tax credit program. As a certified Crisis Care Center through the Missouri Department of Social Services, all tax-deductible donations of $100 or more are eligible to receive up to a 70% tax credit against Missouri state tax liability.

70% NAP Tax Credits FAQs

An individual with business income or a business makes a tax-deductible contribution of cash or stock to Good Samaritan’s Catalyst Program.

Good Samaritan provides donor a 70% tax credit application.

Donor signs, notarizes, and scans application to Good Samaritan.

Donor provides documentation that donation cleared their account. Donor shares documentation with Good Samaritan.

Good Samaritan signs and submits application to Missouri Department of Economic Development.

Missouri DED approves application and sends back certificate to Good Samaritan (processing usually takes 4-6 weeks).

Good Samaritan shares 70% tax credit certificate with donor.

Donor gives certificate and Missouri 2025 Miscellaneous Income Tax Credits form to CPA when they file.

Missouri businesses and individuals that own a business, have rental property, or have a farm operation in Missouri are eligible to claim 70% tax credits. Click here to learn more.

Don’t have qualifying business income? You can still claim 70% tax credits through the Champion for Children tax credit program.

Good Samaritan generally reserves 70% tax credits for donations of $1,000 or more.

There is not a maximum donation amount for 70% tax credits.

Donations can be made by cash, check, credit card, stocks, bonds and other marketable securities as well as real estate.

Note: Donations that include a benefit to the donor will be reduced by that amount, i.e. a meal at a fundraising banquet.

The amount of the claimed tax credit may not exceed the amount of the taxpayer’s state income tax liability for the year the credit is being claimed.

Any tax credit that cannot be claimed in the tax year associated with the contribution may be carried forward and used against a taxpayer’s state tax liability for the following five tax years.

70% CFC Tax Credits FAQs

Missouri individuals and businesses make a tax-deductible contribution of $100 or more to Good Samaritan.

Good Samaritan provides a signed 70% CFC tax credit application to donor.

Donor signs tax credit application.

Donor gives 70% tax credit application and Missouri 2025 Miscellaneous Income Tax Credits form to CPA when they file.

Missouri Department of Revenue collects all 70% tax credit applications. If tax credit ceiling is surpassed, the Department of Revenue will pro-rate the tax credit % among all applications.

All gifts of $100 or more from individuals and businesses in Missouri are eligible for 70% tax credits.

There is not a maximum donation amount for 70% tax credits. However, if the Champion for Children tax credit ceiling is reached, the Department of Revenue will prorate the tax credits among all donors.

All donations of $100 or more are eligible for 70% tax credits.

Donations that include a benefit to the donor will be reduced by that amount, i.e. a meal at a fundraising banquet.

The amount of the claimed tax credit may not exceed the amount of the taxpayer’s state income tax liability for the year the credit is being claimed.

Any tax credit that cannot be claimed in the tax year associated with the contribution may be carried forward and used against a taxpayer’s state tax liability for the following four tax years.

The cumulative amount of tax credits redeemed is two million five hundred thousand dollars for all fiscal years beginning on or after July 1, 2025. This amount is equally divided among the three qualified agencies: CASA, child advocacy centers, and crisis care centers.

In the event the total amount of tax credits claimed exceeds the amount available, the amount redeemed will be apportioned equally among all eligible taxpayers claiming the credit for that agency.

Put another way, there are $833,333 of 70% tax credits available to individuals who donate to Good Samaritan and other “crisis care centers.” If this cap is reached, the percentage of the tax credit is prorated evenly among all individuals who claim the tax credit.

For example, if a donor claims a 70% tax credit through the Champions for Children tax credit program, and the statewide cap is reached, that donor’s tax credit could be decreased from $700 to $645 (the decrease is relative to the gap between the $833,333 available and the amount claimed).If the credit amount redeemed is apportioned and reduced due to lack of available funds, the taxpayer will not be held liable for any penalty or interest, provided the balance is paid or approved payment arrangements have been made, within sixty days of notification. If the balance is not paid within sixty days of notification, the remaining balance, including interest and penalties will be due and payable.”

For more details about tax credits and to see if you qualify, reach out to Colby at cwallace@ranchlife.org.

Any Child - Any Family - Anytime

70% Tax Credits

Your guide to tax credits at Good Samaritan

Through the Neighborhood Assistance Program Tax Credit, you can enjoy a direct credit of 70% of your donation on your Missouri income taxes. These credits are available to corporations and individuals in the state of Missouri that have a business tax liability (Farmers, Landlords, Small-business owners, and more)

70% NAP Tax Credits FAQs

An individual with business income or a business makes a tax-deductible contribution of cash or stock to Good Samaritan’s Catalyst Program.

Good Samaritan provides donor a 70% tax credit application.

Donor signs, notarizes, and scans application to Good Samaritan.

Donor provides documentation that donation cleared their account. Donor shares documentation with Good Samaritan.

Good Samaritan signs and submits application to Missouri Department of Economic Development.

Missouri DED approves application and sends back certificate to Good Samaritan (processing usually takes 4-6 weeks).

Good Samaritan shares 70% tax credit certificate with donor.

Donor gives certificate and Missouri 2025 Miscellaneous Income Tax Credits form to CPA when they file.

Missouri businesses and individuals that own a business, have rental property, or have a farm operation in Missouri are eligible to claim 70% tax credits. Click here to learn more.

Don’t have qualifying business income? You can still claim 70% tax credits through the Champion for Children tax credit program.

Good Samaritan generally reserves 70% tax credits for donations of $1,000 or more.

There is not a maximum donation amount for 70% tax credits.

Donations can be made by cash, check, credit card, stocks, bonds and other marketable securities as well as real estate.

Note: Donations that include a benefit to the donor will be reduced by that amount, i.e. a meal at a fundraising banquet.

The amount of the claimed tax credit may not exceed the amount of the taxpayer’s state income tax liability for the year the credit is being claimed.

Any tax credit that cannot be claimed in the tax year associated with the contribution may be carried forward and used against a taxpayer’s state tax liability for the following five tax years.

Your tax-deductible donation to Good Samaritan may be eligible for 70% tax credits through the Champion for Children tax credit program. As a certified Crisis Care Center through the Missouri Department of Social Services, all tax-deductible donations of $100 or more are eligible to receive up to a 70% tax credit against Missouri state tax liability.

70% CFC Tax Credits FAQs

Missouri individuals and businesses make a tax-deductible contribution of $100 or more to Good Samaritan.

Good Samaritan provides a signed 70% tax credit application to donor.

Donor signs tax credit application.

Donor gives 70% tax credit application and Missouri 2025 Miscellaneous Income Tax Credits form to CPA when they file.

Missouri Department of Revenue collects all 70% tax credit applications. If tax credit ceiling is surpassed, the Department of Revenue will pro-rate the tax credit % among all applications.

All gifts of $50 or more from individuals and businesses in Missouri are eligible for 70% tax credits.

There is not a maximum donation amount for 70% tax credits. However, if the Champion for Children tax credit ceiling is reached, the Department of Revenue will prorate the tax credits among all donors.

All donations of $100 or more are eligible for 70% tax credits.

Donations that include a benefit to the donor will be reduced by that amount, i.e. a meal at a fundraising banquet.

The amount of the claimed tax credit may not exceed the amount of the taxpayer’s state income tax liability for the year the credit is being claimed.

Any tax credit that cannot be claimed in the tax year associated with the contribution may be carried forward and used against a taxpayer’s state tax liability for the following four tax years.

The cumulative amount of tax credits redeemed is two million five hundred thousand dollars for all fiscal years beginning on or after July 1, 2025. This amount is equally divided among the three qualified agencies: CASA, child advocacy centers, and crisis care centers.

In the event the total amount of tax credits claimed exceeds the amount available, the amount redeemed will be apportioned equally among all eligible taxpayers claiming the credit for that agency.

Put another way, there are $833,333 of 70% tax credits available to individuals who donate to Good Samaritan and other “crisis care centers.” If this cap is reached, the percentage of the tax credit is prorated evenly among all individuals who claim the tax credit.

For example, if a donor claims a 70% tax credit through the Champions for Children tax credit program, and the statewide cap is reached, that donor’s tax credit could be decreased from $700 to $645 (the decrease is relative to the gap between the $833,333 available and the amount claimed).If the credit amount redeemed is apportioned and reduced due to lack of available funds, the taxpayer will not be held liable for any penalty or interest, provided the balance is paid or approved payment arrangements have been made, within sixty days of notification. If the balance is not paid within sixty days of notification, the remaining balance, including interest and penalties will be due and payable.”

For more details about tax credits and to see if you qualify, reach out to Colby at cwallace@ranchlife.org.